What is a Credit Score? Why It Matters in India

Introduction

Imagine you’re a salaried professional in Bangalore planning to buy your first apartment in Whitefield or apply for a car loan to beat the city’s traffic. You’ve saved diligently, your income is stable, and you feel ready — but the bank asks for one crucial number before moving forward: your credit score.

For many first-time borrowers, this three-digit number feels mysterious, yet it quietly influences some of the biggest financial decisions of your life. In today’s lending environment — where home loan rates, credit card approvals, and even rental agreements may depend on your creditworthiness — understanding your credit score is no longer optional.

This guide explains what a credit score is, how it works in India (with practical context for Bangalore residents), why it matters, and most importantly, how you can improve it. Whether you’re preparing for a home loan, business expansion, or simply want better financial control, this article will give you clear, actionable insights.

Key Takeaways

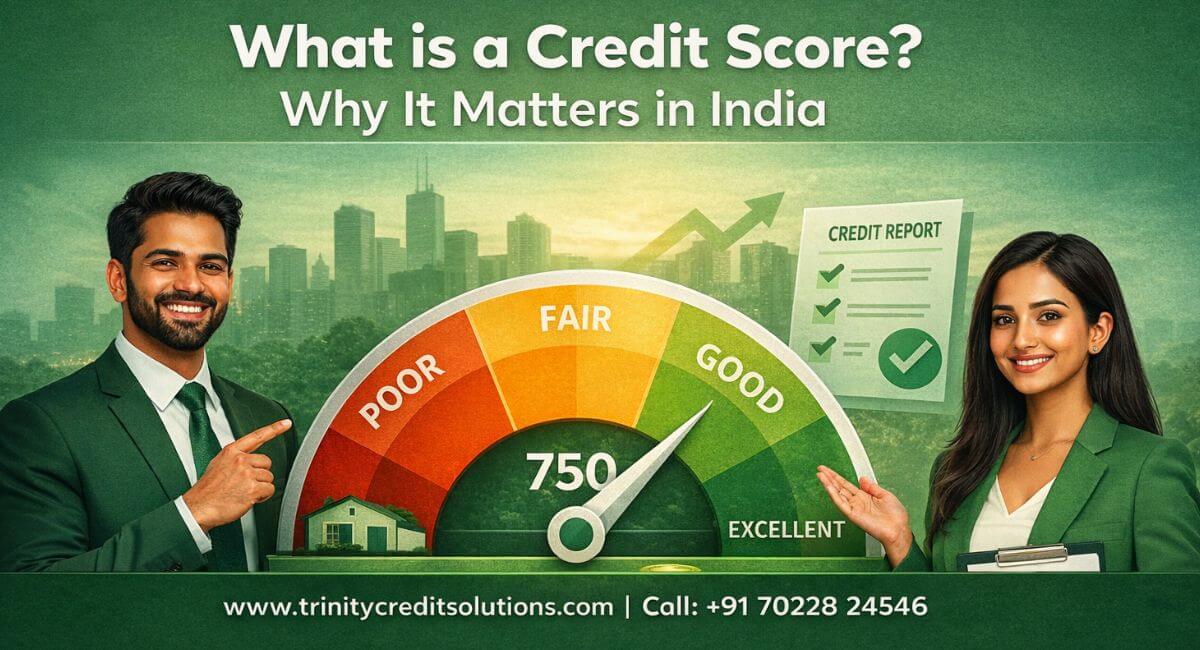

• A credit score is a numerical summary of your credit history, usually ranging from 300 to 900 in India.

• Scores above 750 are generally considered strong by lenders.

• Your score affects loan approvals, interest rates, credit limits, and negotiation power.

• Payment history and credit utilization are the biggest drivers of your score.

• Checking your score regularly helps detect errors early.

• Improving your score can reduce borrowing costs significantly over time.

• Even beginners with no credit history can build a strong profile with simple steps.

• If struggling, guidance from a credit repair agency in Bangalore may help review reports and plan improvements.

Why This Topic Matters

Financial Impact in Real Life

In a city like Bangalore — where property prices are high and lifestyle costs are rising — access to affordable credit can make a major difference. A good credit score can:

• Help secure lower home loan interest rates

• Increase chances of quick loan approvals

• Reduce security deposit requirements in some cases

• Enable access to premium credit cards with rewards

On the other hand, a poor score can lead to higher borrowing costs or outright rejection, delaying important life goals.

Risk Management

Lenders use your credit score to assess risk — essentially, how likely you are to repay borrowed money on time. From a personal finance perspective, your score acts as a financial reputation that follows you across banks and institutions.

Deep Dive — Main Explanation

What is a Credit Score?

A credit score is a three-digit number calculated by credit bureaus based on your borrowing and repayment behavior. In India, major bureaus include:

• CIBIL (most widely used)

• Experian

• Equifax

• CRIF High Mark

Scores typically range from 300 to 900.

How is a Credit Score Calculated?

While formulas vary slightly, most scores consider:

1. Payment History (35–40%) — Timely EMIs and credit card payments

2. Credit Utilization (20–30%) — How much of your credit limit you use

3. Credit Mix (10–15%) — Variety of secured and unsecured loans

4. Credit Age (10–15%) — Length of credit history

5. New Credit Inquiries (5–10%) — Frequency of loan applications

Step-by-Step: How It Works

1. You borrow money or use a credit card.

2. Banks report activity to credit bureaus monthly.

3. Bureaus update your credit report.

4. Your score changes based on behavior.

5. Lenders check the score when you apply for credit.

Detailed Breakdown — Credit Score Ranges and What They Mean

🟢 Excellent (800–900)

• Lowest interest rates

• Fast approvals

• High credit limits

• Strong negotiating power

Example: A tech professional in Bangalore may get preferential home loan offers.

🟡 Good (750–799)

• Strong approval chances

• Competitive rates

• Access to most financial products

🟠 Fair (650–749)

• Possible approvals with moderate rates

• Lenders may ask for additional documentation

🔴 Poor (Below 650)

• High risk from lender perspective

• Limited credit options

• Higher interest costs

Data, Benchmarks, and Industry Insights

• Most Indian lenders prefer a score of 750+ for home loans.

• Credit card approvals often start around 700.

• Borrowers with scores below 650 may face higher rates or require co-applicants.

• RBI guidelines encourage responsible lending, making credit history increasingly important.

In Bangalore’s competitive property market, even a small difference in interest rate (0.5–1%) can translate into lakhs saved over the loan tenure.

How It Affects Outcomes (Costs, Approval, Risk, Benefits)

Interest Rates

Higher scores = lower perceived risk = lower interest rates.

For example:

• Score 780 → Lower EMI

• Score 650 → Higher EMI over decades

Loan Approval Speed

Strong profiles often receive quicker approvals — useful when bidding for property in fast-moving markets like Sarjapur or Electronic City.

Credit Limits

Banks offer higher limits to borrowers with consistent repayment records.

Financial Flexibility

A good score gives you options — balance transfers, refinancing, or negotiating better terms.

Is It Possible with Challenges?

No Credit History (Common Among Young Professionals)

If you’ve never taken a loan:

• Lenders may hesitate due to lack of data.

• Solution: Start with a secured credit card or small consumer loan.

Past Defaults

Even with past missed payments, recovery is possible through consistent repayment over time.

High Debt Burden

You can still improve by reducing utilization and avoiding new borrowing temporarily.

How to Improve Your Credit Score — Step-by-Step

1. Pay Every Bill on Time

Set auto-debit or reminders. Even one missed payment can hurt.

2. Keep Credit Utilization Below 30%

If your limit is ₹1 lakh, try not to exceed ₹30,000.

3. Avoid Frequent Loan Applications

Too many inquiries signal financial stress.

4. Maintain Old Accounts

Longer credit history improves scoring.

5. Check Your Credit Report Regularly

Look for:

• Incorrect late payments

• Duplicate accounts

• Fraudulent activity

6. Diversify Credit Responsibly

A mix of home loan + credit card shows balanced behavior.

7. Reduce Outstanding Debt Strategically

Focus on high-interest loans first.

Expert Tips and Best Practices

• Treat your credit score like a financial asset — protect it proactively.

• Before applying for a home loan in Bangalore, check your score at least 6 months in advance.

• Keep emergency savings to avoid missed payments during job transitions.

• Negotiate with lenders if you have a strong score — they often offer better deals.

• Review reports annually even if you’re not borrowing.

• Avoid closing credit cards abruptly; it can reduce credit age.

Conclusion

Your credit score is more than just a number — it’s a reflection of your financial discipline and a gateway to opportunities. In a fast-growing city like Bangalore, where major life goals often involve borrowing, maintaining a healthy score can save money, reduce stress, and open doors to better financial choices.

The good news is that building or improving your credit profile doesn’t require complex strategies — just consistent habits, awareness, and timely action. Start small, stay disciplined, and monitor progress regularly. Over time, your score will become a powerful ally in achieving your financial goals.

Frequently Asked Questions

Should I close unused credit cards?

Not always — keeping old accounts open can help maintain a longer credit history and support your score.

What lowers a credit score the most?

Missed payments, high credit utilization, defaults, and frequent loan applications significantly reduce scores.

Do credit card payments affect my score immediately?

Changes reflect after lenders report monthly data to credit bureaus, usually within a billing cycle.

Can I get a loan with no credit history?

Yes, through secured loans or entry-level credit products designed for new borrowers.

How long does it take to improve a poor score?

With consistent payments and reduced debt, noticeable improvement may occur within three to six months.

Does checking my own score lower it?

No, self-checks are considered soft inquiries and do not impact your credit score.

How often should I check my credit score.?

Check at least once every three to six months to monitor changes and detect errors early.

What is a good credit score in India?

A score above 750 is generally considered good and improves chances of loan approval with favorable interest rates from most lenders.

Trinity